sponsored by

In a short space of time, discussions around ESG have gone from the fringe to the core of asset management, but this change is the result of decades of groundwork. This month we rewind almost 30 years, to the original meeting of nations in 1992 which laid the foundations for the Conference of Parties (COP) and the shifts in international attitudes that followed. This takes us into intriguing new territory, from hearing how fund managers are dealing with challenging obstacles to finding out what action asset managers are taking to ensure their businesses meet zero carbon aims by the much-discussed 2050 deadline.

Citywire Engage

Get in touch

Chris Sloley Editor, Citywire Selector Rory Vieyra Selector – Sales Manager

Climate action milestones

BURNING ISSUES

What the climate crisis means for fund management

The latest DWS Research Institute report on water investing, published in 2020 and entitled A Transformational Framework For Water Risk, states that an estimated $670bn (€569bn) of annual spending is required until 2030 to meet the sustainable goals associated with water. Yet, the report states, water is the risk where the least progress has been made. According to the report’s authors, who include global head of research, Francesco Curto, head of ESG thematic research, Michael Lewis, and senior ESG strategist Murray Birt, water risk is too often limited to water infrastructure or the protection against waterrelated events such as rising sea levels. But water risk is about the management of water through its entire cycle and its interaction with humans and the environment, the report reads. ‘Direct risk is about access to water, how we use and dispose of it. Indirect risk is about owning an investment indirectly responsible for high water risk activities (financials), or about recognising that water is an input factor in goods and services that we use (food, energy, clothing).’ The authors further argue that equity products have witnessed most progress over the years when it comes to acknowledging water risk. That said, thematic funds are not considered transformational. The report states that these funds often provide exposure to the theme rather than managing the water risk, in the hope that having some ‘water-related stocks’ in the portfolio will mean management of the risk. STREAMS OF CHANGE According to the DWS report, positive approaches and engagement or stewardship approaches have the highest potential to drive change within the water thematic. This positive approach to investment echoes what AllianzGI’s head of thematic equity, Andreas Fruschki, aims to deliver with the firm’s water fund. Citywire A-rated Fruschki’s own Allianz Global Water fund seeks to partake in solving water scarcity and lack of access to clean water. ‘Our water fund is only selecting companies that help improve affordable water supply, preserve water quality or increase water efficiency – this makes the fund both sustainable as well as an attractive means to participate in the growth of water investments which still needs to happen,’ Fruschki said. According to the fund’s latest factsheet, American Water Works is the fund’s largest holding, accounting for 5.86% of the portfolio, with US-based water technology provider Xylem in second place at 4.64%. ‘We run the water fund actively and with high-conviction and prefer to own companies that are pure-plays, i.e. clear beneficiaries of water equipment or infrastructure spending picking up again,’ Fruschki said.

More articles:

2020 was a watershed year, can profit and purpose be sustained?

Chapter 1

Chapter 2

Thirsty for solutions

The investment world has a key part to play in addressing water risk. Specialists in the field talk about how to tap the theme

‘We are entering a decade where growth for water infrastructure is coming from two sources: countries where drinking water from the tap is not yet possible; and from those such as the US, where water infrastructure exists but has an age profile where replacement is needed. American Water Works is very active in replacing and upgrading aged and leaking water networks in the US,’ he added. Meanwhile, the DWS report argues that water infrastructure is both a solution to problems as well as a cause. Traditional water infrastructure is capital intensive, and it has recourse to materials that produce high levels of CO2 emissions, such as steel and cement. Fruschki said water infrastructure is below-surface and out of sight, and it receives less attention than abovesurface infrastructure problems such as traffic congestion, power grids or telecoms coverage. ‘Water leakages can remain unaddressed for many years as replacing water pipes is expensive, creates disruption and can easily be postponed to the next administration. Eventually water main breaks or events such as in Flint in Michigan enter the public awareness and funding willingness improves, which is what we are seeing now,’ he added. EMERGING MARKETS Fruschki said emerging markets have a lot of water-infrastructure needs, but there are few locally-listed companies that are pure plays or have the quality profile in terms of transparency that he would like to see for his water fund. Conversely, UBS Wealth Management selector David Zylberberg said that increased spending in emerging markets supports the water thematic. ‘The attractive business prospects and high revenue visibility of water utilities and the welldiversified business set-up of the waterexposed industrial companies are the main reasons we think investors should include them in their portfolios,’ he said. UBS WM’s private banking selection team has been invested in the water thematic for a while through funds including Pictet Water, Allianz Global Water and Fidelity Sustainable Water & Waste, which the team added to their funds of funds recently. Zylberberg said that the funds complement each other. Thematic water strategies usually vary in the degree of purity of each of the holdings to the water business, or in the way that they relate to benchmarks with the most common water indices. ‘As a private bank we advise investing in a well-diversified investment vehicle that encompasses industrials and utilities alike to ensure reasonable exposure to all key trends, but also offers global exposure to the entire water value chain,’ he added. Zylberberg privileges active management when it comes to selecting thematic strategies, as well as in other types of investments. ‘Investing in the water theme is not as simple as it looks. It is important to understand that the market for water is not dominated by a single sector but comprises several sub-sectors and industries, which are often split into the groups “industrials” and “water utilities”.’ Zylberberg said it is crucial to bear in mind that the water investment theme is less cyclical than many others but that it is not non-cyclical given its exposure to the global industrial sector, which is sensitive to economic cycles. ‘Some sub-sectors, such as smart water systems, show more growth than others that are defined as more value/defensive, such as residential water treatments, or engineering and consulting.’

ANDREAS FRUSCHKI Allianz Global Investors

DAVID ZYLBERBERG UBS Wealth Management

The moment of proof is upon us. How to evidence sustainable change

Protecting the environment is about more than bringing greenhouse emissions down, as managers are finding out with the rise of ‘natural capital’ funds. Nature is one of five key COP26 campaigns in Glasgow this year, with organisers emphasising that agriculture, deforestation and land-use change account for almost a quarter of global emissions and are among the biggest drivers of biodiversity loss. This high-level discussion does not mean that asset managers are sitting idle, as the last 12 months have proved especially productive for the firms engaging with this topic. In its report on stewardship priorities for 2021, BlackRock made the first mention of a natural capital key performance indicator, saying that companies should disclose how their business practices align with the sustainable use and management of natural capital, such as air, water, land, minerals and forests. In January this year HSBC Pollination Climate Asset Management, Mirova and Lombard Odier Investment Managers (LOIM) also formed the Natural Capital Investment Alliance, pledging to mobilise $10bn (€8.5bn) towards natural capital themes across asset classes by 2022. FIGHTING LAND DEGRADATION With so much noise surrounding the natural capital theme, the question remains whether there is a straightforward way to approach it as an investment. This is something that LOIM did some thinking on, as the firm unveiled its first Natural Capital strategy last year with an impressive $400m in assets under management at launch, which was supported by the Prince of Wales. Describing the investment universe of the fund, Christopher Kaminker, head of sustainable investment research at LOIM, said natural capital includes all the renewable and non-renewable resources in our biosphere, including clean air and water, fertile soils and sediments, biodiversity, and finite mineral resources. Kaminker said nature provides enabling and protective services, such as pollination and air filtration, that support economic processes and prevent disruption from climate change, storms, erosion and disease. ‘The $5tn agricultural industry depends as much on rapidlydegrading soils as the forestry industry depends on forests, which are shrinking. We cannot have agriculture without pollination. Bees do not send invoices, after all, despite supporting the pollination of crops worth up to $600bn per year,’ he added. Kaminker singled out Trimble as an example of a company that is helping to decrease the negative impact of agriculture, by connecting GPS information with physical activity. ‘For the farmers, Trimble solutions are a key enabler of smart agriculture. They help them monitor field data and be more precise with fertilisation, water irrigation, but also harvesting. ‘They also provide a high accuracy correction service, delivered via satellite, which is ideal for planting/ seeding, spraying and strip tilling,’ he said.

The core growth areas that LOIM’s nature capital fund is targeting are the circular bioeconomy, resource efficiency, outcomeorientated consumption and zero waste. On the bioeconomy side, the strategy invests in three buckets: biomaterials, which includes renewable packaging firm Stora Enso; smart farming, where sustainable Norwegian fishery Salmar is a pick; and water solutions, such as USbased Advanced Drainage Systems. Explaining the allocation to Salmar, Kaminker said seafood involves 90% less freshwater use, 96% less land use and results in 92% less emissions compared with beef. ‘Sustainable fisheries are all about making sure you don’t destroy the fishing stock beyond how much it can replenish. So sustainable fisheries are an excellent impact investment as well,’ he added. Aside from LOIM’s Natural Capital strategy, there are also funds that are at least in part allocating money along natural capital preservation lines. Robert-Alexandre Poujade, an ESG analyst at BNP Paribas Asset Management, said the firm’s Blue Economy ETF, Circular Economy ETF and Earth fund all take natural capital into account. The firm is also working on a new strategy focused entirely on natural capital. NATURE’S DIVIDENDS The more you look at different strategies, the more it becomes apparent that there are multiple ways to approach investment in natural capital. One firm that looks at this on a more granular level is Earth Capital, which was co-founded by Stephen Lansdown and Gordon Power, two figures behind the British financial services firm Hargreaves Lansdown. Earth Capital has so far invested $1.7bn across agriculture, renewables, data storage and water companies with net positive impact. The firm developed an Earth dividend tool, which applies 30 tests across five ESG dimensions to understand how a given invested company contributes to sustainable development. ‘When we work with companies using our Earth dividend tool, we are trying to minimise the impact of those businesses on areas that push our planetary boundaries into excess,’ said the company’s chief sustainability officer, Richard Burrett. ‘If firms are using natural capital, the question is how to use it more effectively. These are the challenges smart investors are starting to grapple with,’ he added. Earth Capital invests in names such as Noka Farm, a sustainable farming and solar project in Botswana, which could provide 40% of the fresh vegetables sold in the country and be one of the largest independent local power producers. Elsewhere, natural capital and ecosystems is one of the nine sub-themes that Angus Parker, a climate change fund manager at HSBC Asset Management, looks at when considering decarbonisation and energy transition solutions. ‘We are most excited about companies that can both help to reduce the need for further land use change to feed human diets and improve farming practices to ensure a more harmonious relationship between agriculture and nature,’ he said. ENGAGEMENT PRIORITIES Although investors can allocate to certain aspects of natural capital directly, asset managers can also make a difference through voting and engagement. Poujade said BNP Paribas AM is also active on the engagement front. The asset manager supported three water, three forest and three biodiversity proposals in 2020. The biodiversity proposals tackled plastic packaging issues at Walmart, Restaurant Brand International and Kroger. Three forest-linked proposals at Tyson Foods, YUM! Brands and Procter & Gamble addressed supply chain impact on deforestation. BNP Paribas AM is not the only asset manager taking an active stance on engagement here. BlueBay, for example, is contributing to the COP26 process on sustainable land use and trade in forest and agricultural commodities. The asset manager’s head of ESG, My-Linh Ngo, was invited to participate in the global multi-stakeholder taskforce, which will contribute to a dialogue between governments on forest, agricultural and commodity trade. ‘Being involved in this initiative will provide valuable insights into evolving policy dynamics and thinking on best practice, which can support more informed investment decision making. ‘It can also input into our engagement activities with sovereigns and corporates,’ the firm said.

CHRISTOPHER KAMINKER LOIM

ROBERT-ALEXANDRE POUJADE BNP Paribas Asset Management

Back to nature

Fund managers reveal how they are investing in natural capital sustainably

It is far better to drive change from the inside by having open and honest conversations with senior management and the board than to walk away and immediately lose any leverage for change

Lorem ipsum dolor sit amet, consectetuer adipiscing elit

5

Tips on how to improve this integral part of the ESG process

Talk of climate investing always conjures up the big beasts of the transition to a sustainable economy: alternative energy, electric cars, smart cities. However, behind these headline-grabbers, a more nuanced trend is emerging which addresses the fact that climate change is already here and we need to find ways to deal with it. Policymakers are already on the case. COP26 made adaptation and resilience one of its main campaigns, referring to the statistic that climate-related and geophysical disasters are estimated to cost the global economy $520bn each year. Climate change adaptation is also the second of six environmental objectives in the EU taxonomy framework – a classification system establishing a list of environmentally sustainable economic activities. Spread across sectors and geographies, adapters aren’t always easy to identify, but this doesn’t mean investors are not trying to access the space. Piergaetano Iaccarino, head of equity solutions at Amundi, said climate change adaptation solutions are becoming increasingly important to complement more direct ways to invest sustainably, especially where solutions are not available, or require longer timeframes and bigger investments. Amundi’s team is looking across different sectors, including insurance and other financial risk-transfer mechanisms. He said these play a critical part in the adaptation plan, as they aim to reduce vulnerability to the direct impacts of climate change, such as more frequent and more severe extreme weather events. The team has exposure to some of the largest European insurance companies that are heavily investing in this field, including one firm that offers a new parametric risk transfer and assistance service called FastCat. Although Iaccarino couldn’t comment on Amundi’s specific holdings, a quick browse on the internet reveals that French insurer AXA launched such a service in November 2019. ‘FastCat will offer weather alerting and 24/7 real-time assessment using technologies such as satellite imagery and drones, as a way to support communities and corporations facing natural disasters such as floods, earthquakes, cyclones and wildfires, and provide necessary climaterelated insurance products. Notably it will also provide faster claims settlements,’ Iaccarino said. HOME RESCUE Be it Texas storms, Californian wildfires or flooding, housing is one of the sectors that will feel the pain of drastic temperature swings acutely. Anu Narula, a fund manager at Mirabaud, invests in US-based Advanced Drainage Systems as part of the real estate and infrastructure theme within his global equity funds. He said the firm makes drainage structures to manage the flow of urban stormwater using lightweight, recyclable, high-density polyethylene pipes. ‘This reduces the chance of flooding and sewage overflows in extreme weather conditions, using material that is less energy intensive to install, has a longer service life and is more recyclable than its concrete and steel alternatives,’ he added. Narula said there is an estimated $108bn (€91.7bn) funding gap in water and waste water infrastructure in the US, which means Advanced Drainage Systems could also benefit from Biden’s green infrastructure spending. HOTTING UP One of the most visible impacts of climate change is rising temperatures, which we all feel in our homes. Jaime Ramos Martin, manager of the Aviva Investors Climate Transition Global Equity fund, said this is where manufacturers of heating, ventilation and air conditioning systems have a role to play. One company he holds which produces such solutions is Trane Technologies, another US-based business. ‘There is likely to be an increased demand for clean and efficient cooling systems that allow companies and the population to adapt to these temperatures,’ he said.

Shape shifters

Zooming in on the investable companies helping the world adapt to climate change

PIERGAETANO IACCARINO Amundi

Fund managers also see opportunities in the home repair and upgrades space. Jerry Thomas, head of global equities at Sarasin & Partners highlighted Home Depot as a firm that sells products to help people adapt to climate change. ‘Home Depot, the market leader in the home improvement sector for consumers and professionals, is likely to see demand tailwinds for repairs and investment in prevention. ‘Eventually regulation on emissions from residential property will tighten, leading to a need for investment in insulation and lower emissions products for heating and lighting homes,’ he said. A WORLD OF WATER Water management is another climate adaptation topic fund managers bring up within the housing and utilities context. Amundi’s Iaccarino said his team invests in a Japanese company that focuses on curbing flood damage and also provides sophisticated rainwater storage systems to tackle water shortages. Aviva Investors’ Martin holds Xylem, a US-based company that provides products and services to help people use water more efficiently. ‘We believe water infrastructure, both in developed and developing countries, will require substantial investments for a better and smarter use of resources. In our view, the growth opportunity is better than the market anticipates,’ he said. TECHNOLOGICAL EDGE Not all the solutions for more resilient homes are physical. Randeep Somel, manager of the M&G Climate Solutions fund, said an important climate adapter in his portfolio is US software provider Autodesk. The firm’s AutoCAD and Revit software programs are used by architects, engineers and structural designers to design and make models of products and buildings. He said the firm is both a climate solution provider and a climate adapter, as it not only commits to sustainable design practices, but also ensures climate resilience is at the forefront of design and that buildings are capable of withstanding the incoming changes. ‘This is becoming an increasingly important factor in terms of business continuity, safety and insurance,’ Somel added. Although Autodesk is providing software for more resilient buildings, the firm lies within the bigger technology space which is playing its part in climate adaptation. Amundi’s Iaccarino said big data and AI can also contribute to this trend. He referenced the AI for Earth platform provided by a prominent US software company. While Iaccarino did not name the firm, it fits the description of one overseen by Microsoft. Iaccarino said such solutions help to anticipate natural disasters and facilitate more prompt reactions. However, although there are plenty of ideas about tapping the investment potential of climate adapters, some obstacles remain in place. Aviva investors’ Martin said the revenue generation from climate adaptation activities doesn’t always meet his team’s threshold. ‘This is the main issue we face in general. We look for companies with at least 20% of revenues directly related to climate change solutions. This sometimes narrows the options as some of the pure plays tend to be illiquid,’ he said.

ANU NARULA Mirabaud

The ethical investor

The moderate investor

The active investor

The innovative investor

If your client wants their investment portfolio to reflect their strongly held values and beliefs, consider ethical or values-based investing. Some of these funds were originally faith-based and have their roots in religious movements. Others are broader. They will typically use negative screening to remove companies in industries that might be viewed as objectionable from an ethical or moral perspective. They might screen out companies associated with alcohol, tobacco, gambling, pornography, animal testing, weapons and nuclear power, for example. This type of investing is typically quite personalised, as everyone’s moral compass is calibrated differently. What is acceptable to one investor might not be to another.

If your client requires their investments to stick closely to traditional benchmarks but they are happy to screen out the most unsustainable companies, consider an ‘ESG lite’ approach. By investing in the world’s largest companies, there will be some compromises on ESG issues. These companies will not score highly on every factor, although there is a great deal changing, especially since the pandemic. A moderate approach uses negative screening to avoid companies with the lowest ESG scores. This strategy lends itself to investing in less expensive ESG-themed ETFs and index trackers.

If your client wants to choose companies that rank as the most sustainable according to ESG metrics, as opposed to excluding the ones that rank lowest, positive screening could be the best approach. ESG strategies using positive screening seek out companies that are the best in class and score highly on a range of different ESG metrics, including environmental impact, treatment of workers and business ethics. They also use negative screening to exclude companies with the lowest ESG scoring from their investment universe.

If your client wants their investments to support companies creating solutions to world problems, impact investing could be the strategy to follow. The aim of impact investing is to make a positive and measurable impact on society or the environment, as well as generating a financial return. Some impact investing focuses on funding specific projects, such as microfinance funds to create affordable housing, or green bonds to raise money for a clean water initiative. This may mean the portfolio is more concentrated, and there is a good chance it is riskier too. Investors in this space need to be willing to accept more risk and less diversification.

Find an approach to sustainable investing that suits you

Citywire + rated Caroline Shaw is wary about the inherent risks of timber investments. Shaw, who is head of asset management at UK-based Courtiers, started to research the sector in 2012, when a client informed her they had invested a substantial sum of money in a Brazilian teak forest and were about to lose nearly everything, with most of it locked up. Shaw said direct investment into timber is not suitable for retail investors. ‘There is a lack of regulation when it comes to direct timber investing. Investments are typically structured as unregulated collective investment schemes with no recourse to the ombudsman,’ she said. Shaw said history has proven that unregulated products can be tremendously risky, and you need look no further than property funds during the 2008 financial crisis for a prime example. Several unregulated schemes holding property went under and investors had no-one to turn to. ‘The closures are quite horrific for investors,’ Shaw said. For example, in 2017 shareholders voted against a continuation of the Phaunos Timber fund, which forced a realisation of assets, Shaw said. ‘The fund actually closed relatively quickly and investors still lost money.’ Another UK-registered timber-focused investment trust known as Cambium Global Timberland announced it was going to close in 2012. However, as of 2021, the fund is still winding up. ‘This makes me think the investors might not have received much of their cash back. With the last declared NAV at 8.8 pence this has been a disaster for investors who paid 100 pence at launch and have suffered nine years of illiquidity,’ she said.

Barking up the right tree

Investing in sustainable timber is gaining traction as a theme but the nascent sector has inherent illiquidity risks

‘I never want to stand in front of a client and tell them they cannot have some of their money back. That is just not what we do.’ Courtiers serves a mix of clients, including pension funds and high-net-worth (HNW) individuals. ‘We could argue that HNW clients are able to take illiquidity risk, but even wealthy people can be shocked that they can’t get their money back.’ Shaw said it is quite a different story for corporate pension schemes that might want to diversify into illiquid assets and direct investments such as infrastructure. ‘The timeframe enables such investors to hold more illiquid assets.’ LISTED INVESTMENTS Offering something alternative was at the forefront of Christoph Butz’s mind when he launched a timber strategy for Pictet Asset Management in 2008. The Citywire A-rated manager wanted to move away from the traditional equity timber investment approach, which was based on long holding periods and high minimum investment thresholds. ‘We wanted to open up this attractive asset class to smaller institutional and private investors by investing exclusively in stock-listed companies owning timber, which are often traded at hefty discounts to their private equity value,’ Butz said. The Pictet-Timber fund, which holds €672m of assets under management as of February 2021, sits in the top 10 funds within the Equity - Basic Industries sector and has returned 23.8% over the past three years, according to Citywire data. The fund’s latest factsheet said the strategy is invested along the entire forest value chain with a range of holdings including timberland (20.87%), wood products (20.38%), pulp (10.11%), and paper (7.28%). ‘In our view, investing across the value chain makes a lot of industrial sense since it allows investors to benefit from the economic value creation in the processing and transformation of wood, while ensuring a higher diversification in their investment portfolio,’ he said.

CAROLINE SHAW Courtiers

FUNDAMENTAL GREEN SHIFTS According to Butz, the main challenge for timber investing is perception and that a lot of preconceived ideas need to be debunked. ‘Sustainably produced wood is the only renewable material that can help us to significantly lower our fatal dependence on fossil-based materials,’ Butz said. Butz, who joined Pictet AM in 2002 as a sustainability expert, said the whole idea of sustainable development is actually based on sustainable forest management principles that have been evolving over hundreds of years. The Pictet-Timber fund does not invest anywhere near the Amazon rainforest or in other ecologically sensitive areas, or in countries where the governance and forest legislation is too weak and does not guarantee the integrity of the forest. ‘This is the reason why, at this point in time, we are not invested in countries such as Indonesia, Malaysia or Russia, despite their large forest resources,’ Butz said. ‘Timber is a renewable and sustainable resource that provides unique opportunities for a more circular bio-based future economy, but it is only gradually being acknowledged by investors. People have yet to learn that harvesting trees can actually positively impact the climate and the environment,’ he said. The gradual acceptance that timber investment can be sustainable is supported by the rise of numerous reports and white papers on the topic, from the World Bank’s Pension Fund Investment in Forestry (2021), to the S&P Dow Jones indices’ guidelines to understanding Reits sectors, to timberfocused asset managers’ yearly reports. These publications stress the crucial development of third-party ESG certification and potential positive environmental and social impacts. This resonates with Butz’s observation that companies take forest certification very seriously. ‘They have understood that their customers require them to adhere to high standards, and that having certification in place is not only an advantage but a must-have to place their products in many markets today,’ he said.

CHRISTOPH BUTZ Pictet Asset Management

Internationally acknowledged sustainable management standards include the Forest Stewardship Council, the Programme for the Endorsement of Forest Certification, or the European Forestry Commission. The latter covers a broad range of issues, from maintaining high biodiversity and conservation values to community relations, and monitoring the environmental and social impacts of forest management over time, he added. PUTTING DOWN ROOTS Butz intends to benefit from the evolving bioeconomy, which he considers a longterm growth opportunity. ‘The fund focuses on companies that have long-term strategic access to forestland, and that are turning this resource into secular growth products such as lumber and wood panels for greener buildings, sustainable paperbased packaging for plastic substitution or new biomaterials for the new circular bioeconomy,’ he said. In the shorter term, Butz aims to capitalise on the rotation into more cyclical and smallercap value stocks. He also seeks to make use of strong underlying markets and pricing trends, such as the US housing cycle, pulp markets, and ecommerce-driven demand for corrugated packaging. These should provide the backdrop for an ongoing strong performance of the strategy this year, he said. ‘Many of our companies have undergone substantial transformations in their business models since we launched our strategy 12 years ago,’ Butz said. ‘Back then, a lot of these firms were still strongly exposed to conventional printing and writing paper, whereas they are now producing sustainable packaging, pulp or biomolecules for a growing range of applications and products. This transformation is unstoppable, and ultimately also the reason why prices for timberland are bound to continue to move up in the long run,’ he added. Butz’s fund has always had a very low allocation to paper companies because traditional printing and writing paper has faced a secular decline in demand due to ongoing digitalisation. However, he said there is now a lot of innovation and transformation within the paper sector. ‘Ten years ago, companies such as UPM-Kymmene were producing mainly graphic paper, but today they are also producing wood-based biodiesel in Finland, which does not compete at all with the human food chain. UPM-Kymmene is currently building an industrial-scale biorefinery in Germany to produce woodbased ethylene and propylene glycol, which are two of today’s most widely used fossil-based chemical feedstocks for the chemical industry.’

‘If you like forests buy a forest, go enjoy it, walk in it, use it for your own enjoyment, but do not consider it to be a commercial investment’

CAROLINE SHAW

‘We wanted to open up this attractive asset class to smaller institutional and private investors by investing exclusively in stock-listed companies owning timber’

CHRISTOPH BUTZ

BRACED FOR VOLATILITY According to Butz, timber investors have to be prepared to bear a higher volatility compared with broader investments. ‘Prices for timber commodities tend to fluctuate with economic cycles and although there are very different, and sometimes uncorrelated cycles at play, such as housing, pulp and interest rates, it is fair to say that this is not an investment for the faint-hearted. ‘That said, the long-term value of the investment is solidly supported by the tangible underlying value of the forests that the companies hold in the fund, and by robust long-term demand drivers. As such, the unavoidable volatility should really be considered a mere fluctuation, or even an interesting timing opportunity, around a rising and rewarding long-term trend,’ he said. MANAGING INVESTOR EXPECTATIONS According to Courtiers’ Shaw, active management is the only way forward with this type of alternative asset class. ‘By definition, an ETF has to track listed securities – it cannot track an actual forest or invest in an actual forest. Therefore, I do not think that an investor would capture the entire premium they would hope to capture with timber: they would capture a fair amount of equity risk that might override the forestry factor.’ Shaw argues that the crux of this issue lies in managing investor’s expectations. ‘The main concern is not so much to judge if an investment fits a client profile, but rather to manage the client’s expectations and gauge whether they will get the alternative return profile that they were aiming for. ‘When people are investing in forestry, they believe they will invest in an uncorrelated alternative asset. However, that is not necessarily the case, investors might not get what they are led to believe they will get,’ Shaw said. ‘If you like forests buy a forest, go enjoy it, walk in it, use it for your own enjoyment, but do not consider it to be a commercial investment,’ she added.

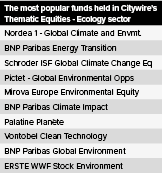

Citywire introduces thematic sectors including ecology, clean energy and wate

Net zero targets are becoming commonplace in company announcements these days, and not surprisingly asset managers are following suit with their commitments. At the end of March this year the Net Zero Asset Managers Alliance announced its expansion by adding 43 new members, which include such heavyweights as BlackRock and Vanguard and together represent $32tn (€27tn) in assets – over a third of invested capital globally. As is often the case with ambitious targets, the key question is whether they are realistic and if firms are backing up their talk with action. Most fund buyers in Europe are currently swamped with demands from the EU’s Sustainable Finance Disclosure Regulation but some have already given some thought to how they want to address carbon neutrality. Rishma Moennasing, head of fund selection and ESG at Rabobank, said her team certainly encourages third-party managers to have net zero ambitions. ‘Our aim is to have an investment portfolio with a carbon intensity which is at least 30% lower than the benchmark and this target might be increased further in coming years,’ she said. However, her team also understands that implementing such a strategy takes time. She added that fund managers have to engage with the underlying companies, and not all firms collect sustainable carbon data or have a policy for carbon neutrality.

Carbon-free finance

An in-depth look at how asset managers and selectors intend to bring their businesses in line with net-zero targets

RISHMA MOENNASING Rabobank

ARE YOU SERIOUS? Luba Nikulina, head of research and a fund selector at Willis Towers Watson, said it is important to differentiate between firms that just make a pledge and figure out their strategy later, and those that map out their route to carbon neutrality thoroughly. She referred to the Institutional Investors Group on Climate Change, which has launched a net zero investment framework and targets. ‘We really like it when asset managers take steps to align with this framework, which is very much in line with governments’ commitment as well. ‘The usual milestones are to try and half your emissions and double green investments by 2030 and then reach the net zero emission target by 2050,’ she said. Some of the strongest signals in her view are when fund managers are thinking about how they are going to measure their portfolios’ emissions. This involves different kinds of metrics, from carbon footprints to how this translates into carbon exposure per dollar invested. ‘A lot of carbon data is backward-looking. We are trying to assess how the landscape is going to change. Thinking about it more in terms of carbon value at risk is really helpful.’ One important element in Nikulina’s view is engagement with underlying businesses, which used to be more prevalent on the equity side but is now increasingly a feature within fixed income. ‘If you are providing new capital, then you should be able to influence how underlying businesses’ assets are being invested.’ This is where she will consider the quality of resources that asset managers devote to engagement and stewardship, and the range of topics that they engage with on underlying businesses. Esmé van Herwijnen, a senior analyst at EdenTree, said asset managers are on the frontlines of the carbon neutrality conversation, as the corporates they invest in are increasingly committed to this goal. She said some asset managers can be tempted into thinking that investing in renewables offsets emissions from other allocations. However, it doesn’t really work like that. ‘I read something where the suggestion was, if you short oil majors that will compensate for the emissions elsewhere in the portfolio. Claiming carbon neutrality by shorting certain stocks doesn’t have any impact on the real world obviously.’

‘I read something where the suggestion was, if you short oil majors that will compensate for the emissions elsewhere in the portfolio. Claiming carbon neutrality by shorting certain stocks doesn’t have any impact on the real world’

ESME VAN HERWIJNEN

BEING A MOTIVATOR Although it is tempting to aim for carbon neutrality by investing in today’s ESG leaders, to make a change in the real economy asset managers will also have to pay attention to ESG improvers. Henrik Pontzen, head of ESG at Union Investment, highlighted that simply avoiding companies with high carbon emissions does not solve the issue of global warming. ‘It is quite possible to measure the temperature of portfolios; if you only invest in financials and IT, you will have an excellent portfolio temperature without solving any problem. ‘Investing in promising transformation candidates can be a far better choice for actually addressing the issue,’ he added. Harry Granqvist, a senior ESG analyst at Nordea Asset Management, holds a similar view. He said investors should always ask themselves when carbon emissions are leaving their portfolios, where are they going? Nordea was one of the co-founders of the Net Zero Asset Managers Initiative. One of its 10 pillars is to prioritise real economy emissions reductions. GET YOUR HANDS DIRTY Granqvist said an approach where investors move away from high-emitting companies towards lower-emitting ones is problematic. To illustrate his position, he gave an example of a hypothetical portfolio with nine software companies and one electric utility company. ‘If I were to divest from that utility company, it would very significantly bring down my portfolio emissions. ‘But in reality what could happen is that the utility firm actually reduces its emissions by 50% next year.’ That’s why he is more inclined to follow the second route and invest in companies that reduce their emissions in line with annual targets under the Paris Agreement. ‘I saw an example of one Swedish pension fund, where more than 100% of the emissions reduction was driven by the allocation effect, while the real emissions actually went in the opposite direction. And that’s clearly a problem.

LUBA NIKULINA Willis Towers Watson

HARRY GRANQVIST Nordea Asset Management

‘If we find ourselves 10 years from now, having achieved a 50% reduction in emissions, but 100% of this is the allocation effect, then we haven’t done well enough.’ Granqvist said that for real reduction of emissions to happen asset managers have to realise that the vast majority of those are going to come from sectors and companies that are emissions intensive and in many cases have a high reliance on fossil fuels. ‘That means we need to be brave enough to stay invested in those sectors, but to actively select the companies that do have credible transition commitments.’ An example, in his view, is Italian utility giant Enel, which you wouldn’t select if you were following the exclusion route. ‘It almost doesn’t matter which climate research institute or sustainability institute we look at, Enel scores on top in basically all of them. ‘When we look at its transition pathway, we see that its emissions reductions targets and renewables conversion rate are compatible with the below two degrees scenario.’ A lot also depends on the sector you are focused on. Granqvist said that when you look at the International Energy Agency’s sustainable development scenario, you get a good understanding of which sectors and regions need to complete the biggest part of their transition. ‘Utilities are on a very accelerated transition path, compared with oil and gas for example, where there is a small group of leaders, relatively speaking,’ he said. Guillaume Mascotto, head of ESG and investment stewardship at American Century Investments, said some energy companies could hold the key to the energy transition. This happened in the past in the case of Ørsted, which was once an oil and gas company that discontinued its dirty assets in 2017 to focus on renewable offshore wind energy. In Mascotto’s view something similar can occur at Total. ‘As part of its ambition to get to net zero by 2050, Total is building a portfolio of activities in renewables and electricity that should account for up to 40% of its sales by 2050 with the objective of being among the world’s top five in renewable energies,’ he said.

GUILLAUME MASCOTTO American Century Investments

CAN YOU WALK THE TALK? One of the biggest challenges when dealing with carbon-heavy companies is to ensure asset managers can adequately track their progress and hold them to account. EdenTree’s van Herwijnen said companies have to show a clear pathway of the steps they are going to take and how they are going to invest in order to meet a particular goal. ‘Is there going to be a huge reliance on offsets by the time we get to 2045, for example, which is clearly not ideal? ‘Or are companies using this 2050 target to slow down the immediate reactions that we need?’ She said EdenTree wants companies to start thinking about residual emissions and if they want to offset those, invest in carbon capture or storage or both. What is not credible, in her view, is setting carbon neutrality targets without clear ambitions to reduce emissions in the first place, which is often the case with oil majors. ‘The announcements made by BP aren’t particularly credible, if it still means they are going to be investing further in new exploration and production, because that simply doesn’t seem to be a sustainable option in the long run.’ She said one example of a good commitment is Danish insulation company Rockwool, which EdenTree invests in. Van Herwijnen said the firm set out a clear set of steps to address energy efficiency and new technology, and is also increasing its work on making processes more circular. ‘We really need to see that research and development, and capex go towards carbon neutrality, rather than a company making one big announcement but then not having a clear strategy about what going to be happening,’ she added.

ESME VAN HERWIJNEN EdenTree

More than 72 asset managers have signed up to the Net Zero Asset Managers Initiative, but that doesn’t mean that the approach to decarbonisation is universal across different investment firms. Union Investment has started with the most critical topic on the path to net zero and is on track to stop investing in coal mining by 2025 and coal-fired power generation by 2035. ‘Now we are discussing how we will proceed with oil and gas, stipulating a path with thresholds and milestones in order to reach carbon neutrality,’ said Henrik Pontzen,head of ESG at the firm. Andy Howard, global head of sustainable investment at Schroders, said you can invest in companies and securities that are themselves aligned to that change on the one hand, while on the other you can encourage the companies in which you are already invested to adapt. ‘Earlier this year, we wrote to the leaders of FTSE 350 companies in the UK, asking them to prepare and publish their plans for the decarbonisation transition ahead. ‘That effort built on the platform of climate engagement we have developed over recent years, starting with our first climate-focused engagement in 2002 and reaching over 200 last year. We plan to push companies to take similar steps in countries beyond the UK.’ Marte Borhaug, head of sustainable outcomes at Aviva Investors, said they are asking firms to set a science-based target aligned with keeping temperatures to 1.5 degrees by 2050. ‘This was also highlighted in our annual letter to company chairs. However, for companies operating in sectors where technology is already available, we are seeing targets brought forward to 2040 and in some cases 2030,’ she said. Borhaug said that to drive change with high-risk companies the firm launched its climate engagement escalation programme this year, which sets out an expectation for 30 of the world’s worst carbon emitters to reach net zero by 2050. ‘There have to be consequences for firms that do not change course and we are prepared to divest holdings in those if they do not show a commitment to material improvement during this programme, which can last for up to three years,’ she added.

Asset managers make it happen

MARTE BORHAUG Aviva Investors

IDENTIFYING THE REAL DEAL What separates leaders from laggards in Granqvist’s view is the quality of the company’s climate governance and transparency. This includes firms disclosing their emissions, the level of responsibility they have for the management of emissions and if they link executive remuneration to climate key performance indicators. Tying climate targets to executive compensation is an appealing solution for Van Herwijnen as well. ‘It doesn’t have to be solely about climate change, but could involve health and safety measures or other indicators that are directly linked to the company’s sustainability strategy,’ she added. Another reason to look at the carbon footprint of portfolios with more scrutiny rather than just removing everything that doesn’t align with the 2 degrees target today, is that this approach might also exclude future climate solutions. Granqvist and the team found that one of the biggest contributors to portfolio emissions is wind turbine manufacturer Vestas, because of the amount of steel and cement that goes into its installations. That’s why Nordea considers this specific investment on a net economy effect basis, as more turbines are needed to reduce the overall emissions of the energy grid. ‘Those are not emissions reductions that will be visible in the company’s own carbon accounting, those are so called ‘avoided emissions,’ he added. Granqvist said that the renewable energy space at least has some guidance on what avoided emissions stand for. In other sectors this metric is less reliable or doesn’t exist at all. ‘Companies tend to get very creative with how they do that. There is no database or scalable technical solution for us to tap into. ‘We have to really understand the narrative for the types of products and services companies provide and what types of data we have to support that narrative.’

TACKLING DATA CHALLENGES Although carbon data is often inconsistent, increasingly fewer asset managers use its shortage as an excuse. This also means that asset managers and asset owners have to do a lot of heavy lifting to educate themselves on the subject. Willis Towers Watson’s Nikulina said the number of pages in business responsibility reports her teams are receiving is increasing. ‘They have overtaken the investment side, and it’s hugely important. However, the risks and opportunities in the space are just incredible. ‘My team spends more than half of its time now on this area, just because there is so much to be done there. I am convinced this is right from an investment perspective and in the best interest of our clients.’ It is just as important, in her view, for investors to educate themselves in climate science. She herself is currently doing some training at Columbia University’s Earth Institute. ‘Asset managers and indeed clients, as well as pension funds, need to elevate their knowledge significantly. ‘This requires time, and when you don’t have much to spare you need to figure out how to become more efficient to create space for this.’ Nikulina said this is particularly challenging for asset owners, who are generally more resource constrained. ADAPT TO SURVIVE Ultimately, the ability of asset managers and asset owners to address the carbon neutrality challenge will come down to their capacity to deal with change. ‘The question is whether both asset owners and asset managers are genuinely skilled in dealing with change and figuring out how to transform themselves over time. It is a massive challenge, but it is about changing mindsets,’ she added. Nordea’s Granqvist said the reality right now is that with many players in the financial industry there is a pretty superficial understanding that emissions are bad and need to be lower. ‘We need to raise the level of understanding in the industry in general. Great things are happening, we are learning together, but there’s a lot of work that needs to be done.’

Smart housing

How investors can capitalise on the boom in sustainable homes

Solutions to achieve energy-efficient housing are rising up investors’ agendas, as countries and companies further commit to decarbonisation targets. Yuko Takano, lead portfolio manager for Future strategies at Newton Investment Management, said French firm Legrand is one of the companies set to benefit from the push towards smart housing.

As long-term investors, we always need to have an eye on sustainability – sustainability of business models, of earnings growth and the ability to manage risk. Sustainability, however, has taken on a new meaning in recent years. It is widely agreed that climate change poses a huge threat to the world - to our societies and economies. Quite simply, without the transition to a low carbon economy, we won’t have sustainable economic growth, and that means we can’t have sustainable investment returns. The global economy has endured a huge hit as a result of the COVID-19 pandemic. We have seen unemployment rates go up and businesses go under. A recent report from the Organisation for Economic Co-operation and Development highlighted that government borrowing in the world’s richest economies surged by a record 60% in 2020, double that of the 2008 financial crisis. More than ever, the world needs greater GDP expansion and less toxic emissions. Fundamentally, lower carbon will mean more growth. But achieving the Paris Agreement of limiting global warming to well below 2°C, preferably to 1.5°C, compared to pre-industrial levels will require substantial investment. But if we do nothing, scientists believe that global temperatures will rise by more than 3 degrees above pre-industrial levels. We know that is going to be very damaging to the environment. It will result in rising sea-levels, extreme weather, societal disruption, the loss of economic activity and more. The energy transition is about moving away from our reliance on the fuels which have driven the global economy for the past 200 years. Instead we need to rely on renewable energy and achieve greater energy efficiency, and this will impact not just power generation but transport, industrial processing, agriculture and the buildings we live and work in. Government backing Governments are thankfully pledging to invest billions into the energy transition – and they are setting themselves some very ambitious targets. In 2020, the European Union unveiled a recovery deal, which included some €550bn earmarked for green initiatives - the biggest single climate pledge ever made, while China, the world’s biggest emitter of carbon dioxide, has committed to becoming carbon neutral by 2060. France has set itself the goal of becoming the first major low-carbon economy in Europe, after announcing a €100bn post-COVID-19 rescue package, of which a third is dedicated to climate-related projects. In addition, New Zealand introduced a law to become mostly carbon neutral by 2050 while Australia, home to some of the world’s largest coal mines, is aiming to have 94% of its electricity generated via renewables by 2040. New US President Joe Biden has yet to set out his stall in full, but climate is high on his administration’s agenda - and he has already said he wants to convert around 645,000 federal vehicles to electric power. In November this year, we have the delayed United Nations climate change conference COP26 in Scotland. In the months running up to it, I anticipate we will hear more governments reiterating their energy plans and carbon reduction targets. Growth opportunities Policy and technology are driving the economics of the energy transition. In our view, the energy transition will be as transformative for the world economy as the digital revolution has been since the 1980s. Over recent years there has been a huge amount of investment into renewable energy. Renewable energy power generation soared by 57% between 2010 and 2018 and the share of renewables in global electricity generation jumped to nearly 28% in the first quarter (Q1) of 2020, from 26% a year earlier. The increase in renewables came mainly at the cost of coal and gas, though those two sources still represent close to 60% of global electricity supply. In Q1 2020 variable renewables – in the form of solar and wind power – reached 9% of generation, up from 8% a year earlier. But the future possibilities are huge. There are going to be significant growth opportunities as a result of this shift away from fossil fuels towards renewable energy. Research shows that clean technology has the potential to drive $1tn to $2tn a year of green infrastructure investments while creating some 15 to 20 million jobs globally and that renewable energy could be the largest area of spending in the energy industry in 2021, surpassing oil and gas. For investors, I believe, there is a need to start adjusting portfolios now. We all need to reset what we think will be the drivers of economic growth over the next decade and beyond. Cutting carbon The reliance on oil and other fossil fuels has led to enormous political problems - even war - over the years. Moving to renewable energy brings immediate benefits. It lowers external costs – costs that are created by economic activity that can affect everybody, such as healthcare costs from heat waves and droughts, and loss of property from flooding. It has been widely recognised that we need to internalise those costs, and this means putting a price on pollution. The costs of renewable energy sources have been coming down dramatically; the levelized cost of electricity from renewable energy – the cost of electricity over the entire life of a power project – is now lower for renewable energies than it is for coal-fired electricity generation. It doesn’t make sense to persist with coal as it’s now more expensive than renewable energy. At the same time the price of carbon is rising. There are various frameworks, or emission trading systems, which aim to put a price on carbon. Companies in certain industries need to pay for the right to generate carbon emissions and the price is going up. There are more of these trading systems being established and they will cover an ever-greater number of global energy and industrial sectors. They are going to help internalise the costs of carbon emissions – if you generate CO₂ you are going to have to pay for it – and you’ll have to pay a higher price in the future. This dramatically changes the economics of some business models and should lead to greater efficiency because of lower, more stable energy costs. The transition It is not easy to replace fossil fuels. Goldman Sachs created a so-called ‘carbon curve’ that estimates the whole range of economic activity that uses fossil fuels – right through the value chain. It then analysed what the cost would be of moving from ‘business as usual’ to replacing primary energy sources with renewable energy. That cost curve eventually gets very steep. For some activities - power generation, agriculture and other land use – this is less problematic and more straightforward. We are witnessing big growth in electric vehicle usage - in fact global sales of electric cars globally actually accelerated by 43% in 2020, to over three million, despite an overall slump in car sales brought on by the pandemic. But while electric vehicles numbers remain small, their uptake is expected to grow. For other sectors - industrial processing, transportation including air and shipping - it becomes very expensive moving to renewable energy. But an abundance of new technology is coming that affects all industries and economic activity. For example, hydrogen technology has barely scratched the surface of its potential as a fuel source for industry and transport, while carbon abatement technology is improving, which is providing lots of growth and investment opportunities. The fact that renewable energy still only accounts for 28% of global electricity generation means we still have some way to go. The cost curve of the transition is ultimately flattening because of the investment we are seeing in new technology, government policy support and the fact that more asset owners are directing capital to carbon reducing technologies. Saudi Arabia is building a brand-new zero emissions city in the desert. It’s going to rely completely on renewable energy and new technologies – it is a real-life experiment to show how we can change the way we live in a more sustainable way. The long-term benefits of the transition As investors, we need to think about the structural trends that will generate economic growth in the future. We believe that means decarbonising portfolios and investing in climate solutions. It means thinking about how to generate earnings growth in the future as business models change and we all benefit from more economic growth and less carbon. Traditional oil and gas producers are adapting their business models - they know that if they do not, they won’t have a future and will be left with stranded assets. We are not going to move to zero oil and gas; companies will still do what they are doing today but they are moving very quickly into the renewable space. We are at the start of a transitioning period towards a lower carbon economy, which doesn’t mean less economic growth - it means more. The costs and risks of doing nothing are much too high. We are on a journey that is going to involve billions, if not trillions, of dollars of investment over the next few years and the technological opportunities that this is going to generate are very exciting. The energy transition will not just create jobs for displaced oil and gas workers, but new positions in new locations, as the placement of these new energy sources become more spread out around the globe. We need economic growth to return but we also need fewer carbon emissions; we all know the dangers presented by climate change. I believe the energy transition can deliver both short-and-long-term benefits; there are huge investment possibilities and massive opportunities in terms of how it affects business models going forward. Investors need to be ready to play their role.

This might be the opportunity to reset and make the kind of intuitional changes and policy choices that will lead to a better, greener and more sustainable future

Chris Iggo AXA IM CIO, Core Investments

Audrey Ryan Support manager, Aegon Global Sustainable Equity Fund

Sponsored content by

Not for Retail distribution: This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly. This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision. Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries. © 2021 AXA Investment Managers. All rights reserved

Aegon Global Sustainability Equity Fund

words by:

An expanding universe of trailblazing instruments

Why less carbon means stronger growth for the global economy

1. Government Borrowing Jumps by Most on Record in Covid Pandemic - Bloomberg 2. https://www.gouvernement.fr/en/european-aspects-of-france-s-recovery-plan 3. Climate Change Response (Zero Carbon) Amendment Act | Ministry for the Environment (mfe.govt.nz) 4. AEMO | Australian Energy Market Operator 5. International Renewable Energy Agency; Renewable Power Generation Costs in 2019. 6. Renewables – Global Energy Review 2020 – Analysis - IEA 7. Goldman Sachs | Insights - Carbonomics: The Green Engine of Economic Recovery 8. Carbonomics The green engine of economic recovery (goldmansachs.com) 9. EV-Volumes - The Electric Vehicle World Sales Database (ev-volumes.com) 10. Saudi Arabia to build a zero emissions city | News | DW | 11.01.2021

1

2

3

4

6

7

8

9

10

Michael Viehs Head of ESG Integration, Federated Hermes

The value of investments and income from them may go down as well as up, and you may not get back the original amount invested. Past performance is not a reliable indicator of future results. For professional investors only. This is a marketing communication. The views and opinions contained herein are those of Anna Chong, Senior Credit Analyst, Andy Jones, Engagement Professional, Sandy Pei, CFA, Deputy Portfolio Manager, Asia ex-Japan, Sonya Likhtman, Engagement Professional, and Stephan Martin, Director, Global Small & Mid Cap, and may not necessarily represent views expressed or reflected in other communications, strategies or products. The information herein is believed to be reliable, but Federated Hermes does not warrant its completeness or accuracy. No responsibility can be accepted for errors of fact or opinion. This material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. This document has no regard to the specific investment objectives, financial situation or particular needs of any specific recipient. This document is published solely for informational purposes and is not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Figures, unless otherwise indicated, are sourced from Federated Hermes. This document is not investment research and is available to any investment firm wishing to receive it. The distribution of the information contained in this document in certain jurisdictions may be restricted and, accordingly, persons into whose possession this document comes are required to make themselves aware of and to observe such restrictions. Issued and approved by Hermes Investment Management Limited which is authorised and regulated by the Financial Conduct Authority. Registered address: Sixth Floor, 150 Cheapside, London EC2V 6ET.

q&a with:

Uncovering attitudes towards sustainable indexing

Steel is essential in today’s world, and it will be just as essential tomorrow – much of the technology to create a zero-carbon future, from wind turbines to mass transportation, will use steel in its construction. Yet steel production itself is a highly polluting activity. One of the most ubiquitous materials in the modern world, steel is used in everything from suspension bridges and skyscrapers to surgical scalpels and cookware. The ready availability of the iron ore from which steel is made and the immense versatility of the finished material have made it integral to the way we live today. Unlike that other great invention of the industrial age, the internal combustion engine, steel looks set to continue its dominance as we transition to a green future: just about every greenhouse gas mitigation technology requires the use of steel, including electrification, thermal energy, and the hydrogen economy. However, producing steel is itself a carbon intensive activity which is responsible for around 7% of energy sector CO2 emissions – or closer to 10% if you include the impacts of mining and transporting the required raw materials (it also accounts for 8% of final energy demand) [1]. Not only that, but the steel industry is a hard to abate sector for which there is no silver bullet currently on offer. Despite the difficulties involved, cleaning up steelmaking will be critical to the wider success of decarbonisation efforts, a fact that governments globally increasingly recognise. Approximately 74% of steel production comes from countries which have a net-zero target in either existing or draft legislation or policy documents, and that figure is only likely to increase [2]. Steel companies therefore face a race to decarbonise before policy changes potentially make their businesses unviable. It is perhaps unsurprising, then, that in recent months four of the top five steel producers have announced intentions to reach net-zero carbon emissions. Collaboration to reduce emissions across the value chain Through our stewardship services team, EOS at Federated Hermes, we engage with companies across the steel value chain on decarbonisation, including mining companies, steel producers and their customers, in particular automotive and construction. We engage with mining companies on reducing their own Scope 1 and 2 emissions through two main approaches: 1. Reducing Scope 1 emissions through the transitioning of dig, haul and rail fleets from diesel to electric, hydrogen and fuel cell electric vehicles (EVs) – for the most part this is a longer-term ambition, although mining EVs including huge dumper trucks are being piloted. 2. Reducing Scope 2 emissions by switching from natural gas and coal to renewable energy sources (especially solar) – this creates net savings and is particularly attractive in the short term. The three routes to decarbonisation In theory reaching net-zero carbon dioxide emission from steel is possible by combining three main routes: demand management, energy efficiency measures, and decarbonisation technologies [3]. As previously mentioned, none of these represent a magic bullet so it makes sense for the industry to pursue all of these solutions in view of the scale of the task. For the industry as a whole, these three routes will go a long way to mitigating emissions in the short-to-medium term. However, even using carbon capture, utilisation and storage in conjunction with these methods is not expected to eliminate all emissions. Achieving the ultimate goal of net-zero steel is likely to require the eventual replacement of blast furnaces with electric arc furnaces, potentially supplemented by the adoption of electrolysis production. Feedstock for these electric arc furnaces will ideally come from scrap, with hydrogen-produced DRI potentially making up any shortfall until scrap supply can meet demand. Decarbonising the steel industry is far from a simple task, but it is an essential one if we are to achieve a zero-carbon future. To read more about how the international business of Federated Hermes engages with companies across the steel value chain, read the full edition of Spectrum – decarbonising the global steel industry. [1] “Iron and Steel Technology Roadmap,” published by the IEA in October 2020. [2] This is calculated by the international business of Federated Hermes using World Steel Association data from 2020 production by country and Net Zero Tracker | Energy & Climate Intelligence Unit (eciu.net). [3] Energy Transition Commission.

A burning issue: decarbonising the global steel industry

For nearly 30 years, when the Janus Henderson Global Sustainable approach began, we have recognised the link between sustainability and innovation, and today we believe we are entering a decade of transformational change. The transition to a low carbon economy is finally accelerating. We view decarbonisation as a generational investment trend that will have a profound impact on almost every sector of the economy. What does low carbon investing mean? Low carbon investing is much more than simply investing in renewable energy companies and removing fossil fuels from a portfolio. For the last 250 years, since the beginning of the Industrial Revolution, humankind has made tremendous progress using a fossil fuel-driven economic growth engine. Unfortunately, tremendous industrial progress has not come without its consequences. The world today relies heavily on the use of carbon-emitting processes in everyday life, such that it would be hard to live without them. In essence, the fossil economy has been woven into our global economic system. Greenhouse gas emissions are produced across almost all industries. The largest emitters include transportation, electricity, power generation, industry, commercial and residential buildings, and agriculture. However, it is important to consider that the fossil fuel economy is a highly complex and interdependent system, as shown in figure 1. Within each sector are various sub sectors and industries with differing levels of fossil fuel-driven economic activity. Detangling the web of carbon-emitting processes is no easy feat.

Hamish Chamberlayne Portfolio Manager/Head of Global Sustainable Equities at Janus Henderson

Author:

A long-term highly active, growth-focused approach to sustainable investing

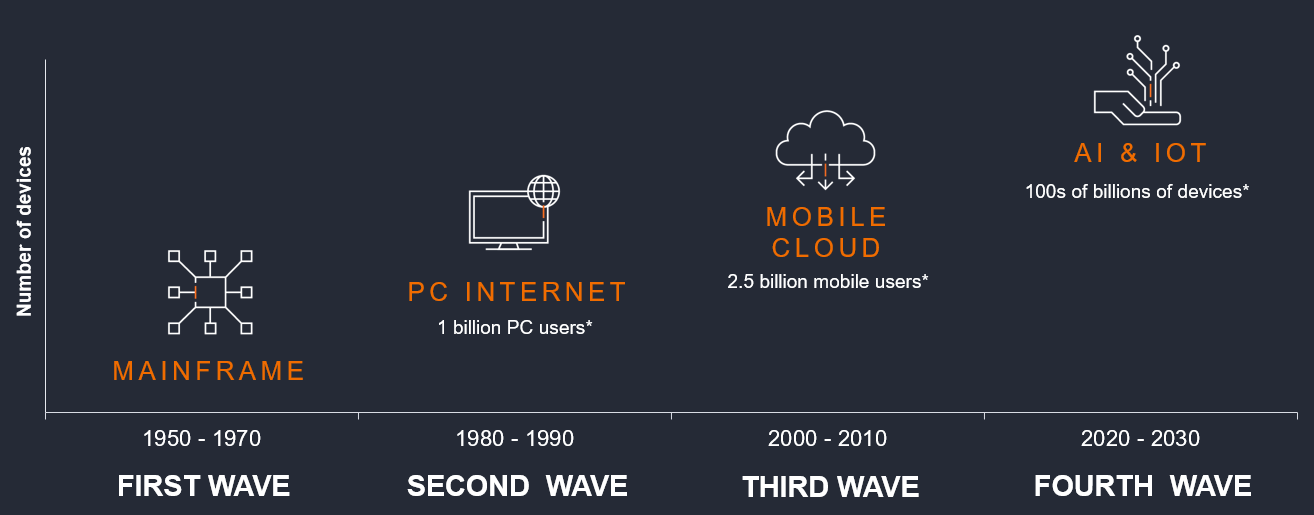

‘Renewable, electric, digital’: the Fourth Industrial Revolution

Figure 1: Global greenhouse gas emissions by sector

Synchronised investment boom into clean technologies This year, the world’s most influential governments have made ambitious commitments to tackle climate change head on. In April, 40 world leaders convened virtually to address the climate crisis at the Leaders Summit on Climate. The White House stated its aim to reduce US emissions by 50-52% by 2030 based on 2005 levels and China premier Xi Jinping announced intentions to phase out coal use from 2026. Meanwhile, the UK government announced the world’s most ambitious climate change target to cut emissions by 78% by 2035 compared to 1990 levels. The UK's sixth carbon budget is set to include international aviation and shipping emissions and would bring the UK more than three-quarters of the way to net zero by 2050. Today, we are pleased to see much greater global political harmony on the climate agenda. The stars are aligning for what we believe will be a globally synchronised investment boom into clean technologies. So, what do these climate commitments mean for the fossil fuel economy? In order to align with the 1.5oC climate limit, we will need multiple solutions to address the multiple sectors and industries involved. Countries must increase electricity share of the primary energy mix from 20% to 50% over the next few decades. The US has set out material provisions to electrify a portion of the school bus fleet, retrofit buildings to higher environmental standards, reduce the use of coal and gas generation and invest in the country’s electric and renewable energy infrastructure. The UK, meanwhile, has banned the sale of diesel and petrol cars by 2030 and announced a £20m funding pot for electric vehicles. A decade of transformational change Electrification of the global automotive fleet is one area that we are particularly excited about. As battery and computing technology continues to improve and associated costs decrease, we expect to see mass production and adoption of electric vehicles. This is often referred to as the S-curve. When plotted on a chart, the S-curve illustrates the innovation of a technology from its slow early beginnings as it is developed, to an acceleration phase as it matures and, finally, to its stabilisation over time. The electrification of vehicles is just one example of this. We believe we are standing at the beginning of a decade of transformational change that will induce multiple S-curves across many different industries. At the heart of this change is electrification. Picture a light emitting diode (LED) bulb, which emits light through a process called electroluminescence. In contrast to the traditional incandescent bulb, which emits light through the heating of a small metal filament, LEDs pass electrical currents through semiconducting material in order to emit photons. This same photon emitting process can be used to transmit data. LiFi, similar to WiFi, is a wireless communication technology which utilises the LED process to transmit data from one object to another. While the details of LiFi might be fascinating, the key takeaway is that the electrification and digitalisation are intrinsically linked. As electrification continues to develop, everything will become ‘smart’ and connected, blurring the lines between sectors and industries. Over the next decade, we anticipate the inception of multiple S-curves as technology improves and connectivity progresses. Traditional analogue products will make way for the new era of cloud computing and the Industrial Internet of Things. This shift has already started happening in smart cars, smart watches and even smart fridges. We consider this to be the Fourth Industrial Revolution (see figure 2).

Figure 2: The Fourth Industrial Revolution: merging industrial and technological economies

Source: Climate Watch, The World Resources Institute, 2020. Global greenhouse gas emissions data from 2016.

Source: Janus Henderson Investors, 2021. *Citi Research, as at 31 December 2016. Note: AI = artificial intelligence, IOT = Internet of Things.

The fourth industrial revolution is enabling us to move from a ‘fossil analog’ economy towards a ‘renewable electric digital’ economy. It is at the heart of decarbonisation and the transition to a low carbon economy. We refer to the trio of digitalisation, electrification and decarbonisation (DED) as the ‘DED nexus’. These dynamics are impacting every sector and every corner of the global economy. As investors, we highlight the importance of considering the implications of these changes on portfolios. The DED nexus has been accelerated by the events of last year and we believe that, combined, they are powerful agents of positive change with regards to both societal and environmental sustainability goals.

Disclaimer Copy...................................................

Learn more about the Janus Henderson Global Sustainable Equity approach. Click HERE

Important information